As the effect of the Trump administration’s fluctuating tariff policies have heightened uncertainty for consumers and the markets, economists have begun to worry about the looming risk of stagflation, an economic condition not seen in the United States since the 1970s. Though the U.S. economy is still in a “strong position” according to the Federal Reserve’s latest assessment, the agency raised its inflation forecasts and lowered projections for growth.

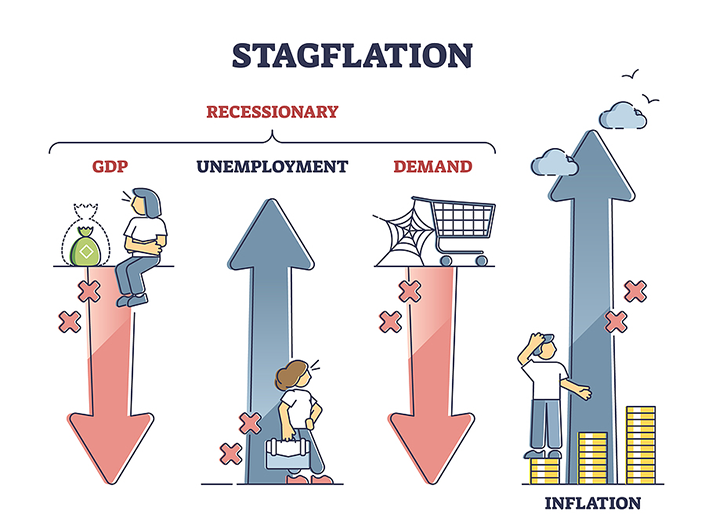

The term stagflation, a blend of “stagnation” and “inflation,” was invented by the colorful conservative British politician and expert bridge player Iain Macleod in the 1960s during a period of economic distress in the United Kingdom. (Macleod also coined the term “nanny state”). Macleod’s portmanteau phrase was widely adopted by economists and politicians to refer to the combination of high inflation, stagnant economic growth, and elevated unemployment.

Because stagflation includes hits to the economy from various angles, it can be difficult to recover from and can lead to long-term recession. For example, if an economy is experiencing only inflation, deflation can address the issue and help the economy recover. But if stagflation is at play, deflation may not spur fast recovery; deflation alone doesn’t address slow growth and unemployment issues.

Warning Signs

“A stagflation trend was already in place before tariffs,” said Adam Phillips, managing director of investments with EP Wealth Advisors. Smith was alluding to some recent signs of softer economic growth and continued inflation. “To the extent that tariffs remain in place, that will only exacerbate the problem,” he said.

Fed chair Jerome Powell noted on May 7 that the “risks of higher unemployment and higher inflation appear to have risen.” Those two factors—along with slower economic growth—are the very definition of stagflation, hence the alarm bells.

The labor market remains in the same healthy spot it has been for the past six to eight months, Powell said. But the more than 30,000 federal jobs cut since President Trump took office aren’t yet reflected in government data.

On June 3, 2025, the Paris-based Organization for Economic Co-operation and Development (OECD), an intergovernmental agency devoted to stimulating economic progress and democracy formed by 38 developed nations in North America, Europe, South America, plus Japan and Australia, downgraded its growth forecasts for both the U.S. and global economy.

After saying in March 2025 that U.S. growth was expected to have a 2.2% expansion the OECD outlook was downwardly revised to 1.6% for 2025 and 1.5% in 2026. Global GDP growth was projected to slow to 2.9% in 2025 and 2026, with “the slowdown … concentrated in the United States, Canada and Mexico.” The OECD had previously forecasted global growth of 3.1% in 2025 and 3% in 2026.

“The global outlook is becoming increasingly challenging,” the OECD report said. “Substantial increases in barriers to trade, tighter financial conditions, weaker business and consumer confidence and heightened policy uncertainty will all have marked adverse effects on growth prospects if they persist.”

OECD Chief Economist Alvaro Pereira told CNBC that “trade uncertainty and economic policy uncertainty has reached unprecedented levels.”

The OECD also adjusted its inflation forecast, saying “higher trade costs, especially in countries raising tariffs, will also push up inflation, although their impact will be offset partially by weaker commodity prices.” The inflation projection for the U.S. was set at 3.2%, up from a previous 2.8% projection, with a warning that U.S. inflation could even be closing in on 4% toward the end of 2025.

Fear and Loathing

Investors don’t like inflation because it erodes the present value of future earnings, a different and often more substantial headwind for stocks. They don’t like slow economic growth because that means slower earnings growth, as well, which is a headwind for equity prices. If you combine the two—slow growth and higher inflation—you get the worst of all worlds. So, investors absolutely hate stagflation.

In theory, a weak economy with rising unemployment undercuts inflation, so the two should not coexist. But as with oil-price shocks in the 1970s that drove prices higher, the tariff shock anticipated from the Trump administration’s trade policies now has the world guessing. Some investors remain concerned that import levies could bring stagflation, where rising costs collide with weak economic growth. If the tariffs remain in place for any length of time on the magnitude of what is already being proposed and considered, that’s a recipe for much slower growth and much higher inflation.

Consumers are also wary. Consumer sentiment surveys show an increase in overall expectations of inflation, which reflects concerns that the Trump administration’s policies could lead to stagflation rather than growth. As tariffs push up prices and weaken purchasing power, consumers are likely to buy less, which creates a reaction of stocks falling and yields rising. The White House has promised tax cuts and other stimulus measures, but households seem to see rising prices and a squeeze on disposable income arriving ahead of any tax relief.

With inflation still around 2.3% and on-off reciprocal tariff policies being announced daily, there remain several months for supply chains to adjust, with some of that adjustment passing through as higher prices for consumers. A study of 2018 tariffs showed that prices rose immediately, but there was retaliation and potential impacts on other non-tariffed goods. This suggests that higher prices will filter through for the remainder of 2025, long enough to keep asset prices under pressure due to stagflation fears. Any tax cuts enacted during this time would only serve to add to inflationary pressure.

The Conference Board’s Consumer Confidence Index experienced its largest monthly increase in over four years in May, marking the first monthly rise since November. Consumers were less pessimistic about business conditions and job availability over the next six months and regained optimism about future income prospects. Consumers’ assessments of the present situation also improved. However, while consumers were more positive about current business conditions than last month, their appraisal of current job availability weakened for the fifth consecutive month.

University of Michigan’s consumer sentiment measure was unchanged from April, ending four straight months of declines, and remaining at the fourth lowest reading on record. Sentiment had ebbed at the preliminary reading for May but turned a corner in the latter half of the month following the temporary pause on some tariffs on China goods. Expected business conditions improved after mid-month, likely a consequence of the trade policy announcement. However, these positive changes were offset by declines in current personal finances stemming from stagnating incomes throughout May. Overall, consumers see the outlook for the economy as no worse than last month, but they remained quite worried about the future.

Gloom and Doom

Souring sentiment has already prompted several economists to cut their outlooks on the U.S. economy. Guidance from blue-chip U.S. companies has been deteriorating as well. This negative outlook will put downward pressure on earnings regardless of what country bears the tariffs costs.

Walmart, long a barometer of U.S. consumer strength, announced it will raise prices on items including electronics, toys, and some grocery foods as the global trade war increases the company’s costs. “We will do our best to keep our prices as low as possible,” said Walmart CEO Doug McMillon on a May 15 earnings call. “But given the magnitude of the tariffs, even at the reduced levels announced this week, we can’t absorb all the pressure given the reality of narrow retail margins. The higher tariffs will result in higher prices.”

Walmart finance chief John David Rainey told CNBC that same day: “You’ll begin to see [higher prices], likely towards the tail end of this month, and then certainly much more in June.”

The Wall Street Journal reported that foreign travel to the U.S.’s main airports declined 6% in May 2025 from the same period last year, with airline bookings data for the summer of 2025 suggesting a further slump. Flight bookings to the U.S. from Europe are down by about 12% through August 2025. Amid this decline in travel to the U.S. from Canada and Europe as well as a fall-off in domestic bookings, U.S. airlines including American, Delta, and Southwest have slashed their forecasts.

Supply-chain issues for high-demand products could soon soar. The New York Time reported that the Chinese government on April 4, 2025, halted all global exports of rare earth metal magnets as part of its trade war with the U.S. Once produced in American factories until production was moved to China in the early 2000s by manufacturers to save on labor costs, these magnets are converted from rare earth metals and used to power everything from cars and semiconductors to fighter jets and robots.

While the relationship between consumer confidence and spending is weak, economists said the continued deterioration should not be ignored, adding that it aligned with their forecasts for slow economic growth and high inflation this year.

Conclusion: Is a 1970s Style Coming Back?

We expect to see some rebounds in the second quarter 2025 consumer spending reports, which will reflect the change in weather and consumers’ rush to buy various goods, including big purchases such as autos, before prices go higher.

However, if consumers retrench in reaction to tariff-induced price increases, the economic outlook in the second half of 2025 could significantly weaken. Capital spending is also likely to get hit during the second half of this year.

Tariffs are a particularly difficult economic threat for the Federal Reserve to address. The agency’s mandate is to keep inflation low and stable while maintaining a healthy labor market. Tariffs represent a “supply shock” that both raises inflation, which calls for higher interest rates, and hurts employment, which calls for lower rates. Bouts of uncertainty trigger fight or flight reactions. That has resulted in a toxic mix of panic and paralysis.

The Fed would have to choose which threat to emphasize. In 2024, Fed officials thought they might have engineered a “soft landing,” which refers to bringing inflation down without causing a recession or a significant rise in unemployment. Now, the agency is publicly warning of a stagflation scenario.

Other nations’ central banks have also raised the risk of stagflation and the need to keep policy restrictive once it occurs. Powell said the Fed was not in that place yet, but such a scenario would raise challenging issues for the agency. If push comes to shove, the Fed will hold rates higher for longer to slow inflation, instead of instituting stimulating policies to avoid an increased, more pernicious bout of inflation.

The last time the U.S. experienced stagflation, in the 1970s, the Fed oscillated between hiking rates to combat inflation and lowering them to combat high unemployment, a “stop-go-stop” policy that is now widely viewed as a failure because neither inflation nor unemployment was satisfactorily contained.

It may be difficult for the Federal Reserve to combat stagflation since the Fed usually raises rates when it is worried about high prices and lowers rates when a weaker job market is a bigger economic concern. With both scenarios at play, the agency’s hands may be tied.

The economy has been resilient over the past three years in the face of the tightening of monetary policy. But at Bowen Asset Management, we are losing confidence that the economy can remain durable in the face of layoffs and tariffs. We are expecting the economy to slow.

However, the big questions remain: When will the economy slow down? How much will it slow? And, as many are wondering, will we tip into a recession?

As always, if you have any questions about this report or any other questions, please reach out to Bowen Asset at info@bowenasset.com or (610) 793-1001.

Disclaimer

While this article may concern an area of investing or investment strategy in which we supply advice to clients, this document is not intended to constitute a complete description of our investment services and is for informational purposes only. It is in no way a solicitation or an offer to sell securities or investment advisory services. Any statements regarding market or other financial information is obtained from sources which we and/or our suppliers believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information.

Past performance should not be taken as an indicator or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. As with any investment strategy or portion thereof, there is potential for profit as well as the possibility of loss. The price, value of and income from investments mentioned in this report (if any) can fall as well as rise. To the extent that any financial projections are contained herein, such projections are dependent on the occurrence of future events, which cannot be predicted or assumed; therefore, the actual results achieved during the projection period, if applicable, may vary materially from the projections.